Based on the latest NIQ reports and research data for 2025–2026, the Greek retail market is defined by a cautious, value-driven consumer base navigating a landscape of high market concentration and rapid innovation.

1.Consumer Sentiment and Financial Status

Greek shoppers are experiencing a significant economic divide compared to global averages.

Financial Pessimism: 47% of Greeks feel they are financially worse off compared to a year ago, significantly higher than the 33% global average.

Recessionary Mindset: 61% of consumers believe Greece is currently in a recession, with 76% of those expecting it to last at least another year.

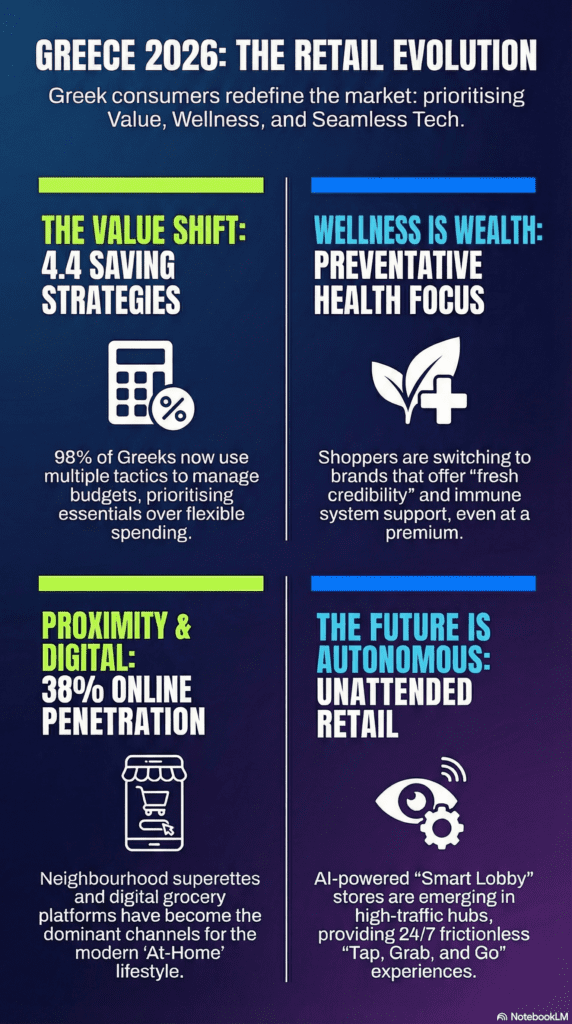

Spending Limits: 57% of Greeks report they only have enough money for the basics, while “free spenders” represent only 3% of the population.

2026 Outlook: Households are regaining control but not abandoning caution; “multi-saving behaviour” has become the new normal.

2. What Greeks Want: Core Purchasing Drivers

Value and health are the primary engines of choice in the current market.

Value-Centric Store Choice: Store choice is primarily driven by pricing, promotions, and value-for-money (VFM).

Freshness and Quality: Shoppers prioritise “fresh credibility” and product variety, which reinforces loyalty to top retailers.

Preventative Health: There is a major shift toward preventative health strategies. Greeks are willing to pay more for products that are free from preservatives and artificial colours or support their immune systems, provided they still taste great.

Greek Origin: Both domestic (43%) and inbound (41%) tourists actively seek and choose products of Greek origin.

Innovation-Led Growth: 32% of the overall FMCG assortment has been renewed in the last three years. In fact, new items are the sole growth driver for non-food categories.

Private Label (PL) Solidification: PLs are firmly embedded in baskets, holding a 24.3% value share. While initially driven by price, rising quality perceptions in essentials are validating PL competitiveness.

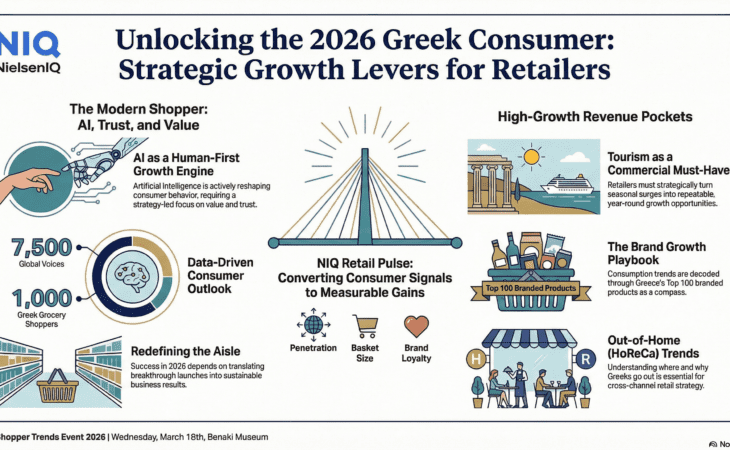

The Tourism “Retail Economy”: Tourism has become a daily retail engine. Domestic tourists behave like “temporary residents,” with 95% buying food from supermarkets. Inbound tourists prepare a large share of their snacks (65%) themselves, creating a high-value retail opportunity for portable and impulse-friendly items.

Retail Consolidation: The market is increasingly top-heavy. Sklavenitis remains the clear leader in equity, while Lidl gains momentum through price image and AB stands out for loyalty benefits.

AI Integration: AI recommendations are noticed by 75% of online shoppers. Greeks value AI most for price-based and time-sensitive recommendations that help them save money.

4. Where We Are Going: 2026 and Beyond

The retail landscape is shifting toward proximity, digital integration, and intentional consumption.

Consolidation of Formats: Growth is led by Superettes (+9.1%) and Hypermarkets (+8.8%), while traditional channels like Kiosks are struggling (-5.4%).

Market Dynamics: Although total turnover surpassed €16.2 billion in 2025, FMCG volumes remain near levels from 20 years ago, while the Average Basket Price has increased by 30%.

Home-Centric Consumption: Consumers are shifting toward purposeful, not spontaneous out-of-home behavior. 47% are visiting food and drink establishments less frequently, leading to a trend of consuming more at home.

Autonomous Retail: Retailers are focusing on intelligent convenience amenities to capture the “on-the-go” mission as traditional kiosks decline.

5.The Top Products they Buy !

While shoppers remain deeply attached to daily rituals and core brands, they are increasingly strategic, balancing financial caution with a selective openness to innovation and wellness-oriented products.

1. The Core Basket: Rituals and Top Products

Greek consumption is anchored in specific categories that drive supermarket traffic and turnover.

The Dominance of Beverages: All of the top 10 branded SKUs in Greece are beverages, accounting for nearly 25% of the total turnover of the top 100 products.

Top 10 Branded SKUs (by Value):

Loumidis Papagalos 200gr (Greek Coffee)

Nescafe Classic 200gr (Instant Coffee)

Nounou Family 3.6% fat 1500ml (Fresh Milk)

Alfa Lager 6X330ml (Beer Multipack)

Johnnie Walker Red Label 700ml (Whisky)

Coca Cola Zero 6X330ml

Vikos Mineral Water 6X1500ml

Loumidis Papagalos 100gr

Coca Cola Zero 2X1500ml

Nescafe Classic 100gr.

Ritualistic Categories: Coffee is not viewed as a mere category but as a ritual, with Greek and instant coffee dominating through high loyalty. Similarly, Milk and Dairy remain essential store drivers due to their high penetration and frequency of purchase.

2. Innovation and “The New Aisle”

Greek consumers are showing an increasing willingness to try new things, even while managing tight budgets.

Assortment Renewal:32% of the overall FMCG assortment in Greece has been renewed in the last three years.

Growth Drivers: In Non-Food categories (Household, Health & Beauty), market growth is exclusively attributed to new items.

Breakthrough Success: A notable example of successful innovation in 2025 was the Ion Break Dubai Style Pistachio Kataifi chocolate, which became one of the top-performing new launches.

3. The Wellness and Quality Shift

Greeks are increasingly adopting preventative health strategies, prioritising wellness in their baskets.

Pricing Power of Wellness: 70% of shoppers in 2026 make a point of buying healthy options. Consumers are willing to pay a premium for products that are free from preservatives, artificial colours, and flavours, provided they still taste great.

Greek Origin: There is a strong preference for local products; 43% of domestic tourists and 41% of inbound tourists specifically look for and choose products of Greek origin.

4. Strategic Saving and Private Labels

Economic pressure has turned “multi-saving” into the new normal for Greek households.

Saving Strategies: 98% of consumers employ at least one saving strategy, with an average of 4.4 strategies per shopper. The most common tactic is substituting branded products for lower-priced alternatives (40%).

Private Label (PL) Growth: PLs now hold a 24.3% value share of the market. While price remains the primary entry driver, quality perceptions are rising, with shoppers increasingly viewing PL quality as being “just as good” as named brands in essential categories.

Promotional Intensity: Greeks rely heavily on promotions; branded FMCGs see a promotional intensity of 66.7%.

Tourism has evolved into a “daily retail economy” where travellers act as temporary residents.

Domestic Travellers: 95% purchase food categories during their holidays, with a heavy focus on breakfast and snacking items to support self-catering in Airbnbs and holiday homes.

Inbound Travellers: 72% purchase food items, but their primary focus is on beverages (94%), specifically bottled water (82%) and beer (41%).

Non-Food Essentials: Travellers also drive significant volume in Personal Hygiene (36%) and Suncare (17%).

6. Where the Money Goes: Retailer Leadership

Spending is highly concentrated among a few top retailers. Sklavenitis remains the clear national leader in store equity and consolidation, followed by Lidl, which continues to gain momentum through its price image, and AB, which leads in perceived loyalty benefits. Growth is currently most robust in Superettes (+9.1%) and Hypermarkets (+8.8%), while traditional kiosks are in decline.

Start Free for up to 20k euros in revenue from Recommendations!

Test out the Recommendation Engine for up to 20.000 euros in revenue from recommendations. No credit card required. Just enter your company information and we’ll contact you with all the details.

We use technologies like cookies to store and/or access device information. We do this to improve browsing experience and to show (non-) personalized ads. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.