This comprehensive study, based on the NIQ 2025–2026 Shopper Trends and Retail Pulse reports, provides a strategic roadmap for retailers across diverse sectors—including Clothing, House appliances, Pharmacies, delivery etc—to navigate a Greek market defined by economic divide, habitual loyalty, and technological acceleration.

NIQ’s Retail Pulse is an annual, syndicated survey-based solution that leverages a decade of trended data across more than 50 markets to decode the evolving retail landscape and store performance.

The 2026 Greek edition was based on a random sample of 1,037 main grocery buyers and influencers aged 18–65, providing comprehensive national coverage across key regions including Attica, Thessaloniki, and Crete.

This study serves as a strategic “pulse” for the industry, helping leaders convert demand signals into measurable gains in penetration and loyalty by understanding the motivations behind store choices and shifting shopper attitudes.

In the FMCG sector, the findings reveal a market that reached record heights, surpassing €16.2 billion in turnover in 2025, with growth currently being volume-led at +5.9%.

However, while turnover is rising, actual volumes remain near levels from 20 years ago, and the Average Basket Price has increased by 30%.

Beverages remain the primary engine of the market, accounting for nearly 25% of the turnover of the top 100 branded products. Private Labels (PL) have also solidified their role, maintaining a 24.3% value share as quality perceptions of these products now rival named brands. Crucially, innovation is the sole driver of growth in non-food categories, with 32% of the total Greek FMCG assortment being renewed in just the last three years.

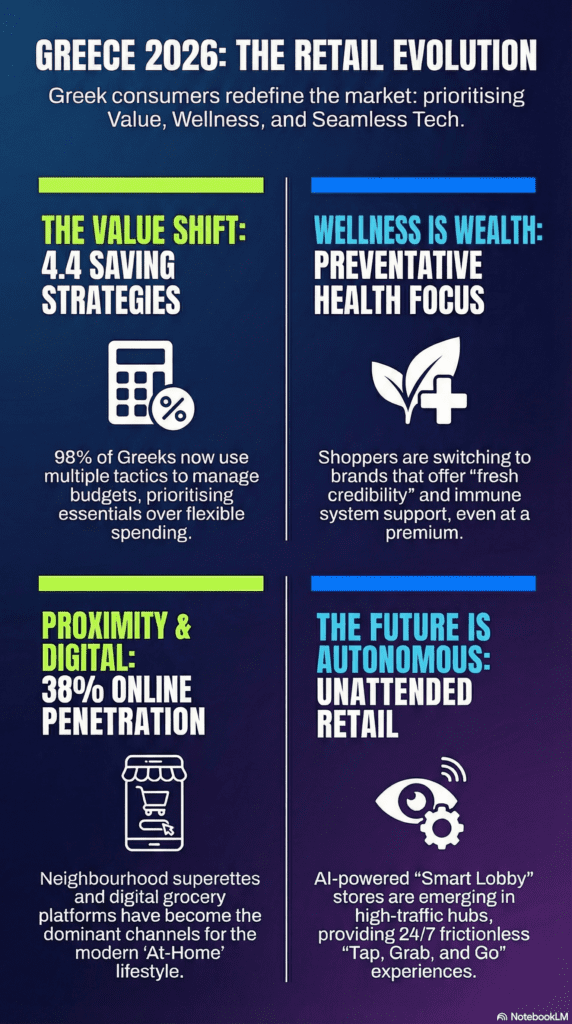

This shifting behaviour will force all retailers to adapt to a consumer base that is now permanently in “multi-saving mode,” with 98% of Greeks employing an average of 4.4 distinct strategies to manage their budgets.

Retailers must navigate a highly concentrated, top-heavy market where leaders like Sklavenitis dominate through availability and “fresh credibility,” while the “Battle for the Neighborhood” intensifies, evidenced by small-format superettes leading growth at +9.1%.

Furthermore, a significant move toward preventative health means 70% of shoppers now prioritize healthy options, and the rise of digital integration—with online grocery penetration at 38%—requires retailers to provide frictionless, price-transparent experiences both on the shelf and through mobile apps.

1. The Macro-Economic Context: A “Basics-Only and Healthy ” Reality

Before addressing specific sectors, it is vital to understand the financial climate of the Greek consumer.

The Recessionary Mindset: Despite organized trade reaching record turnovers (€16.2bn in 2025), 61% of Greeks believe they are in a recession, with 76% expecting it to last another year.

Spending Limits: 57% of Greeks report having money only for the basics, and 47% feel financially worse off than a year ago.

Multi-Saving Mode: 98% of consumers employ saving strategies, using an average of 4.4 tactics (e.g., substituting brands, buying in bulk, or hunting for promotions).

Universal Advice: Every retailer, regardless of sector, must position themselves as a Value-for-Money (VFM) ally. Luxury and spontaneity are being replaced by intentional spending.

In the non-food sector, growth is driven by one primary engine: Innovation.

The Innovation Mandate: NIQ findings show that growth in non-food categories is exclusively attributed to new items.

Wellness as a Premium: Greeks are shifting from reactive to preventative health strategies. This is a massive opportunity for athletic retailers. Consumers are willing to pay more for products that support physical wellness.

Advice:

Assortment Renewal: Keep your catalog fresh. 32% of successful retail assortments in Greece have been renewed in the last three years.

Health Utility: Market athletic clothing not just as fashion, but as essential equipment for a preventative health lifestyle.

AI Personalization: Use AI for style-based recommendations and time-sensitive deals, which 75% of online shoppers notice and value.

B. House Appliances & Furniture

The Greek household is refocusing on the home-centric lifestyle.

The “At-Home” Trend: Consuming and living at home is the dominant projected behavior for 2026 [source turn 1].

Value Multi-packs & Durability: Shoppers favor “Bigger packs, bigger baskets” to save money in the long run.

Advice:

Energy Efficiency as VFM: Given the high inflation in production costs (noted as a top risk by 47% of C-suite executives), appliances that reduce long-term household bills should be marketed as a “saving strategy”.

Showrooming vs. Online: Online grocery penetration is at 38%; furniture and appliances must follow this “complementary” channel model where the website provides transparency and price comparison, which Greeks highly value.

C. Pharmacies & Personal Care

Engagement with pharmacies and personal care stores is increasing.

The Hygiene Shift: “Guarantees of safety and hygiene” are the #1 driver for Greeks when choosing which brands to trust.

Premium for “Free-From”: Consumers will pay a premium for products free from preservatives, artificial colors, and flavors.

Advice:

Stock the “Clean” Aisle: Prioritize natural and immune-supporting supplements, as these are top growing categories.

Reliability: In the online space, “online safety” and “reliable delivery” are top drivers for pharmacy-adjacent products.

D. Restaurant Delivery (HoReCa)

The “Going-Out” pulse is changing due to stricter regulations and financial pressure.

Purposeful Consumption: Greeks are visiting food establishments less frequently (47% decrease in frequency) [source turn 3].

Café & Fast Food Dominance: Cafés and fast-food outlets lead the out-of-home pulse, with most visits occurring during the day or at “similar times” to last year.

Advice:

The Q-Commerce Expectation: Quick-commerce adoption is at 37%, raising expectations for immediacy. If you deliver, it must be fast.

Promotional Bundling: Use “Deals & promos” (a top AI-driven benefit) to encourage group orders, catering to the “multi-saving” mindset.

3. The Digital Advantage: Artificial Intelligence

Greeks are highly familiar with AI (85%) and use it more than the EMEA average for shopping.

What they want from AI: Practicality. They seek price-based recommendations (58%) and time-sensitive offers (52%).

Trust vs. Control: While 70% trust AI assistant recommendations, Greeks demand transparency and the ability to opt out.

Advice for all Retailers:

Integrate “Discovery Nodes”: Turn your digital platform into a “Moment of Discovery”.

Optimize for “Basics”: Use AI to help consumers find the best value for their “basics-only” budget.

Efficiency: Use AI to improve on-shelf availability, which is a critical driver for store loyalty.

4. Winning the “Tourism Retail Economy”

Tourism is no longer just for hotels; it is a commercial must-have for all Greek retail.

The Temporary Resident: Both domestic and inbound tourists rely on local shops for more than just souvenirs. They buy personal hygiene (36%), suncare (17%), and Greek origin products (41%).

Advice:

The “Greek Origin” Label: Clearly mark products of Greek origin. 43% of domestic travellers actively choose them [source turn 2, 96].

Proximity is King: Small-format stores and “Superettes” are growing at 9.1% because they win the “Battle for the Neighborhood”. Ensure your footprint is where the tourists (and residents) actually live.

To succeed, Greek retailers must bridge the gap between ritualistic habits and strategic innovation.

Lead with Value: Promotions are not an option; they are the baseline. Branded FMCGs have a promotional intensity of 66.7%.

Innovate or Stagnate: Companies with growing innovation sales are 2x more likely to grow overall sales.

Execute with AI: Use technology to save the consumer time and money, the two most valued benefits in the current climate.

Capture the Home: As “At-Home” becomes the dominant 2026 behavior, position your products (furniture, apparel, food) as essential components of a comfortable, value-driven domestic life [source turn 1, 90].

By focusing on speed-to-shelf, price transparency, and preventative wellness, retailers can convert the current economic uncertainty into a period of sustainable consolidation and growth.

Start Free for up to 20k euros in revenue from Recommendations!

Test out the Recommendation Engine for up to 20.000 euros in revenue from recommendations. No credit card required. Just enter your company information and we’ll contact you with all the details.

We use technologies like cookies to store and/or access device information. We do this to improve browsing experience and to show (non-) personalized ads. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.